Annual Percentage Rate: How It Impacts You

When you are shopping for a loan, the Annual Percentage Rate (APR) is one of the most important things to understand. The APR is the monthly cost you pay to borrow money, including fees, expressed as a percentage. It’s a broader measure of the cost to you of borrowing money since it reflects not only the interest rate but also the fees that you have to pay to get the loan. So, how does APR impact you? Let’s take a closer look.

Some Background

What Is An Annual Percentage Rate?

An annual percentage rate (APR) is a yearly rate that includes interest and other costs associated with a loan. For example, when you get a mortgage, you may be quoted an APR of 5% and told that the interest rate on your loan will be %. The X% APR includes the Y% interest rate and certain other costs associated with your loan, such as credit evaluation and processing fees charged by the lender.

What Does It Mean To Me?

The APR is important to you because it is the true cost of borrowing money. The interest rate alone doesn’t give you the full picture. APR was actually developed to help in comparing loans. It’s important to compare APRs when you’re shopping for a loan, rather than just looking at the interest rate. That’s because the APR gives you a more complete picture of the cost of borrowing money.

For example, let’s say you’re considering two loans: Loan A has an interest rate of 4.0% and an APR of 4.2%. Loan B has an interest rate of 4.0% and an APR of 5.0%. Which loan is cheaper? The answer is Loan A. Even though the interest rates are the same, the APR for Loan A is lower, so it’s the cheaper option.

When you’re looking at loans, always compare APRs to get the full picture of the cost of borrowing money.

Formulas And Other Fun Stuff

How To Calculate Nominal (Stated) Interest Rate

You don’t need a calculation! Stated interest rates are the interest rate listed on a loan, savings account, bond, or other financial instruments.

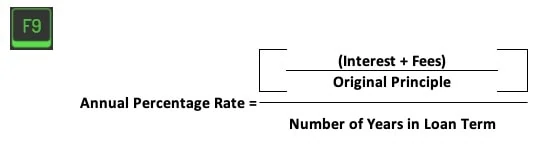

How To Calculate Annual Percentage Rate

To calculate the APR on a loan, you need to know the:

-Total interest paid over the life of the loan (Stated interest rate compounded over the life of the loan)

-Fees charged by the lender

-Original principal

-Term of the loan

From there, add up the total interest and fees, divide it by the principal, and divide again by the number of years. Simple as that!

Finding Information on Interest Rates

When it comes to interest rates, the internet is your best friend. Almost every financial institution explains its interest rates and compounding programs. To that end, if you’re looking for a good place to start, try Googling “Interest Rates + Your City/Country.” This should give you a variety of resources with information on interest rates in your area.

Let’s Walk Through An Example

Let’s Recap

When you’re shopping for a loan, it’s important to compare Annual Percentage Rates (APRs) in order to get the full picture of the cost of borrowing money. This is because the APR includes not only the interest rate but also other costs associated with the loan.

Frequently Asked Questions

What Is The Difference Between APR and AER?

The Annual Percentage Rate (APR) is the actual rate of interest that you pay on your loan. This rate includes any fees or charges associated with the loan. The Annual Equivalent Rate (AER) is the rate of interest after taking into account the effects of compounding to normalize the interest rate.

What Is A Good APR Rate?

This depends on a variety of factors, including the type of loan, the current market conditions, and your personal financial situation. In general, however, lower interest rates are better than higher interest rates.

What Is The Difference Between APR and APY?

The Annual Percentage Rate (APR) is the actual rate of interest that you pay on your loan. This rate includes any fees or charges associated with the loan. The Annual Percentage Yield (APY) is the effective yield of an investment, taking into account the effects of compounding.

Have any questions? Are there other topics you would like us to cover? Leave a comment below and let us know! Make sure to subscribe to our Newsletter to receive exclusive financial news right to your inbox.