ASC 210: Basics of the Balance Sheet

ASC 210, also known as the Balance Sheet topic in the Accounting Standards Codification, is a bit like a GPS for your business finances. It provides a roadmap that helps you understand exactly where your business stands financially at any given point in time. Think of it like taking a financial selfie – it’s a snapshot that shows what your business owns (these are called assets) and what it owes (we call these liabilities).

Now, you may be wondering, “Why do I need to understand this?” Well, imagine setting off on a road trip without a map or GPS. You could end up anywhere, right? Similarly, understanding ASC 210 helps you navigate the financial journey of your business. It guides your decisions, keeps you on track, and helps you avoid any nasty financial potholes.

Key Takeaways

In accounting, a balance sheet is one of three core financial statements (along with the income statement and the cash flow statement) that provides a snapshot of what a business owns (assets), owes (liabilities), and the amount left for the owners (equity) at a specific point in time.

ASC 210 guides the presentation of balance sheets. It outlines the criteria for classifying assets and liabilities as current or noncurrent, rules for offsetting, and requirements for disclosure about the liquidity of an entity, among other things.

The four main purposes of a balance sheet are: to provide a statement of financial position at a specific point in time, to aid in understanding the company’s liquidity and financial flexibility, to provide information for calculating financial ratios and making financial projections, and to provide a basis for investors, creditors, and other stakeholders to make decisions.

Accounting Rules And Regulations

Companies are subject to different accounting rules based on where they are based. In the US, companies must follow Generally Accepted Accounting Principles (GAAP), which are a set of standardized principles and guidelines for financial accounting used by public companies. One of these principles is ASC 210.

In essence, ASC 210 requires businesses to prepare their balance sheet following GAAP, which ensures consistency and accuracy in financial reporting. It also sets guidelines for what should be included in the balance sheet and how it should be presented.

The Financial Accounting Standards Board (FASB) maintains GAAP. The board issues new rules as necessary to ensure that GAAP remains up-to-date. FASB provides free online access to the Accounting Standards Codification (ASC), which is the only authoritative source to research US GAAP. FASB and the AICPA also provide access to other authoritative literature that supplements the GAAP Hierarchy.

Other countries follow the International Financial Reporting Standards or IFRS. IFRS is similar to GAAP, but there are some key differences that businesses need to be aware of if they operate globally. Under IFRS, balance sheets are covered by the International Accounting Standard (IAS) 1, which outlines the presentation of financial statements.

Understanding the Balance Sheet: ASC 210-10

Alright, now that we’re all buckled up and ready to hit the financial road, let’s start with an essential part of our journey – understanding the balance sheet. Just like how a photo captures a moment, a balance sheet is a financial statement that captures your business’s financial health at a specific point in time. It’s an instant snapshot that shows you exactly where you stand.

Think of it like planning a road trip. Before you set off, you need to know your starting point, your destination, and what you have in your car – snacks, gas, your favorite playlist.

In a similar vein, a company’s balance sheet tells you what your business has (assets), what it owes (liabilities), and what’s left for you (equity).

The balance sheet equation is Assets = Liabilities + Shareholder Equity

Now, let’s talk about assets. These are the things your business owns. Imagine them as the snacks in your car for your road trip. They could be cash, inventory, equipment, or even money others owe you. Liabilities, on the other hand, are what your business owes. Picture these as the miles you need to cover on your trip. They could be loans, rent, salaries, or invoices you need to pay.

This brings us to ASC 210-10. This section guides how to present your balance sheet properly. It’s like your GPS, guiding you on how to pack your car efficiently for your road trip. It helps you categorize and organize your assets and liabilities so that anyone glancing at your balance sheet can quickly understand your business’s financial status.

So, how do we create a balance sheet? Let’s break down the balance sheet accounts:

Assets

Start by listing all of your company’s assets. Remember to include both current assets (like cash, prepaid expenses, and accounts receivable) and long-term assets (like property and equipment).

Liabilities

Next, jot down all debts and obligations. Again, separate current liabilities (due within a year) and long-term liabilities (due beyond a year). This includes everything from accounts payable and loans to pension fund liability.

Shareholders Equity

Here’s the fun part – think of it as finally reaching your destination. Subtract your total liabilities from your total assets. This gives you your equity, or what’s left for you after all debts are paid. This section is further broken down into paid in capital and retained earnings.

Navigating Offsetting: ASC 210-20

Now that we’ve got a good handle on the balance sheet, it’s time to throw a little curveball into the mix – but don’t worry, we’re going to tackle this together! This curveball is called “offsetting,” and it’s a concept that can really change the game when it comes to understanding your business’s financial picture.

Offsetting, in the world of finance, is kind of like having a coupon for your favorite store. Let’s say you owe the store $100, but you have a coupon for $20 off. In reality, you only owe $80, right? Similarly, offsetting in finance means deducting related assets and liabilities against each other, showing the net balance on your balance sheet.

This is where ASC 210-20 steps in. It’s like the rulebook that tells you when you can use your coupon. According to this guideline, you can only apply offsetting when you have the legal right to offset the recognized amounts and intend to settle on a net basis or to realize the asset and settle the liability simultaneously.

Let’s illustrate this with a real-life example. Imagine you have a loan from a bank for $10,000 (a liability), but you also have $4,000 deposited in a savings account at the same bank (an asset). If the bank agrees, you can offset the deposit against the loan, reducing your liability to $6,000. This reflects a more accurate picture of your company’s health.

So how do we apply these offsetting rules to a balance sheet? Here are the steps:

- Identify Offsetting Opportunities: Review your assets and liabilities to see if there are any opportunities for offsetting. Remember, both must be with the same party, and you should have the legal right to offset.

- Apply Offsetting: Deduct the smaller amount from the larger one. For example, if you have a liability of $10,000 and an asset of $4,000 with the same party, your offset liability would be $6,000.

- Update Your Balance Sheet: Replace your original asset and liability amounts with the new offset figures.

How To Review A Balance Sheet

When reviewing a balance sheet, using financial ratios can provide valuable insights into a company’s financial health. These ratios can help assess the company’s liquidity, leverage, and how much financial risk exists. Here are some key ratios to consider:

- Current Ratio: This is calculated by dividing current assets by current liabilities. It measures a company’s ability to cover its short-term obligations. A ratio of 1 or higher indicates that the company has enough assets to cover its short-term liabilities.

- Quick Ratio: Also known as the acid-test ratio, it’s calculated by subtracting inventory from current assets and then dividing by current liabilities. This ratio provides a more stringent assessment of a company’s short-term liquidity by excluding inventory, which might not be easily convertible to cash.

- Debt-to-Equity Ratio: This is calculated by dividing total liabilities by shareholders’ equity. It measures the degree to which a company is financing its operations through debt versus wholly-owned funds. A high ratio may indicate that the company has taken on a lot of debt, which could be risky.

- Return on Assets (ROA): This is calculated by dividing net income by total assets. ROA measures how effectively a company is using its assets to generate profit. A higher ratio indicates greater efficiency in managing assets to produce earnings.

- Asset Turnover Ratio: This is calculated by dividing net sales by average total assets during the period. It measures how efficiently a company uses its assets to generate sales. A higher ratio suggests better asset utilization.

Remember, these ratios should not be viewed in isolation but rather used in comparison with industry peers or the company’s historical performance. This will give you a more comprehensive understanding of the company’s financial position and performance.

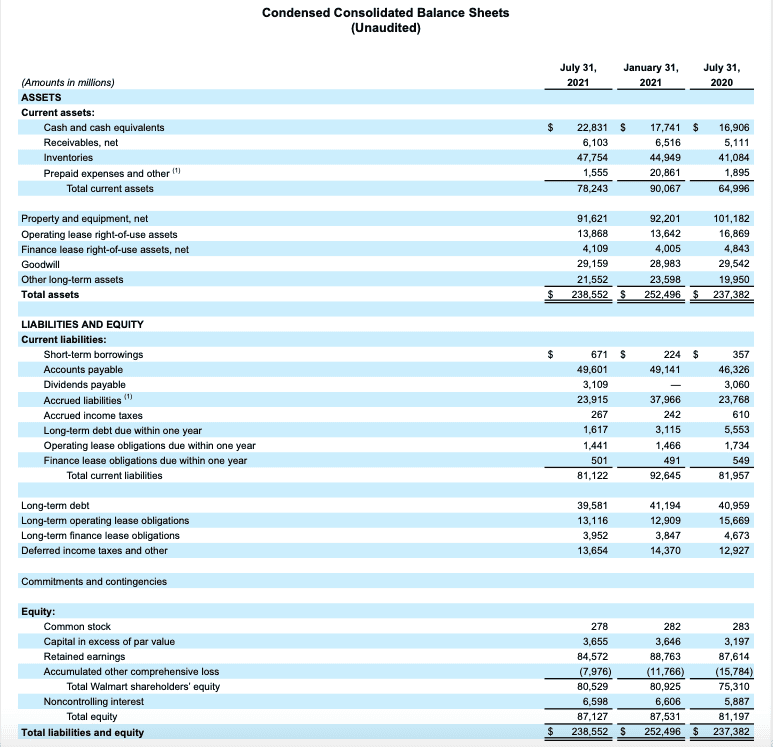

Balance Sheet Example

Here is a sample balance sheet from Walmart

And here is another balance sheet example from Coca-Cola

Frequently Asked Questions

How do you reclassify a negative cash balance?

A negative cash balance is typically reclassified to the liability section of the balance sheet under ‘overdrafts’ or ‘short-term borrowings.’ This reclassification provides a more accurate depiction of the company’s financial position.

What is the right to offset ASC 210?

The right to offset, according to ASC 210, refers to the ability to deduct related assets and liabilities against each other, resulting in a net balance on the balance sheet. This can only be done when there’s a legally enforceable right to offset the recognized amounts, and there is an intention to settle on a net basis or realize the asset and settle the liability simultaneously.

What is the difference between a classified balance sheet and an unclassified balance sheet?

A classified balance sheet categorizes assets and liabilities into current and non-current sections, providing more detailed information about a company’s liquidity and financial flexibility. On the other hand, an unclassified balance sheet lists all assets and liabilities in order of liquidity without segregation into current and non-current sections.

Have any questions? Are there other topics you would like us to cover? Leave a comment below and let us know! Make sure to subscribe to our Newsletter to receive exclusive financial news right to your inbox.